2027 Rate Changes - Massachusetts: +13.1% indy, +12.7% sm. group, +12.9% avg (preliminary)

Thu, 06/11/2026 - 11:18am

Via the Massachusetts Division of Insurance:

2027 Health Insurance Rates

In accordance with the provisions of 211 CMR 66.08(3)(e), and in order to ensure that insurance rates are fair to consumers, the Division of Insurance reviews and seeks public comment on the rates requested by health insurance carriers.

The following tables depict the proposed overall weighted average premium increase and the key assumptions behind premium development for the merged (individual and small employer) market filed by insurance carriers as part of the Massachusetts Division of Insurance rate review process (for rates effective in 2027). This information is subject to change as the rate review process continues.

The Health Care Access Bureau within the Massachusetts Division of Insurance is currently reviewing these assumptions. This review process will culminate in a final decision in August 2026.

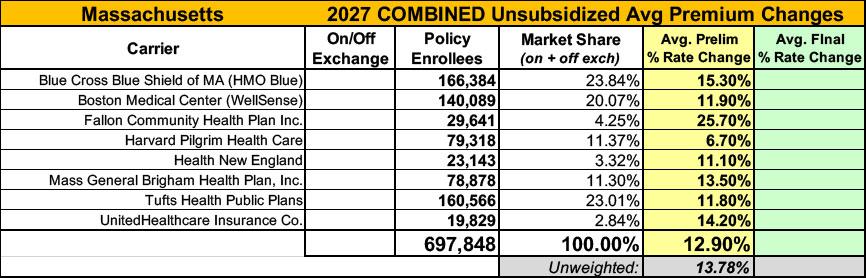

Merged Market Summary for Proposed Rates Effective for 2027

The Average Rate Change represents adjustments to reflect benefit changes in renewing plans and it reflects plans that have been terminated and mapped to existing plan offerings. This weighted average rate change represents the average rate change consumers will experience before changes due to age.

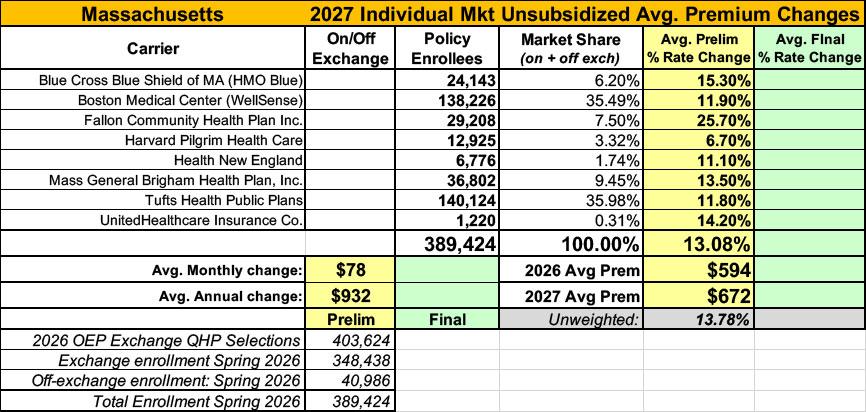

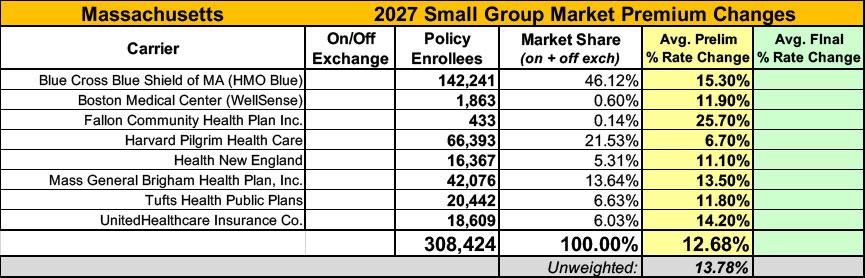

Unlike most states, Massachusetts has a merged individual & small group market risk pool, which means that rate changes to both are based on combined data. The carrier filings still break out how many enrollees each have in their individual vs. small group plans, however, which still allows me to run the weighted average rate hikes for each market separately.

Across both markets, there's ~698,000 enrollees with a weighted average requested rate hike of 12.9%. If you break it out into the indy & small group markets, it's 13.1% for the former vs. 12.7% for the latter.

Blue Cross Blue Shield of Massachusetts HMO Blue, Inc.

Costs for medical care and medications for our members have escalated rapidly and spending is now growing at the fastest rate in more than a decade. The surge in spending is putting a heavy burden on our employer customers and members who are struggling to keep up with rising costs.

We’ve seen use and severity trend accelerate through the end of 2025. This is not an anomaly, but rather reflects observable, sustained increases in underlying medical utilization and severity identified by our Trend Analytics Team. We are experiencing persistent utilization pressures across multiple service categories, most notably in outpatient surgeries (including digestive and cardiovascular surgeries), rising behavioral health visit volumes, and increased medical pharmacy use.

We have also observed and measured an increase in the severity component of trend. We have measured the impact of changes in the way providers are billing both inpatient and outpatient services to increase provider revenue with no appreciable difference in the way care is delivered. As recent state reports have found, hospital and pharmaceutical costs continue to be the two largest categories of medical spending increases across Massachusetts. The effects of inflation and labor shortages have led to large price increase requests from healthcare providers. Additionally, more than 30% of total medical expense trend is driven by pharmaceutical costs.

The impact of blockbuster high-cost biologics, and other innovative emerging therapies has a material impact on current trends. These dynamics put added pressure on medical claims, which in turn causes premiums to increase.

There are several other factors that drive medical spending, including the proliferation of new and expensive technology, an aging population, and the increased utilization of expensive specialty drugs.

Boston Medical Center Health Plan, Inc. (BMCHP) d/b/a WellSense Health Plan (WellSense)

The overall average annual premium rate change is 11.9%, which is driven by the factors outlined below:

- Higher medical and pharmacy Trend:

- Medical costs continue to increase, partly due to provider contracting dynamics. Providers often seek higher reimbursement for ACA commercial plans to offset lower government-mandated rates from public programs.

- In addition, the Connector’s 2024 Seal of Approval requirement to align provider networks across metal tiers has increased WellSense’s provider costs. Changes to certain subsidized ConnectorCare plans in 2026 have also shifted members into products with higher reimbursement levels, further contributing to cost increases.

- Behavioral health, while still a smaller share of total spending, has experienced rapid growth - exceeding 20% annually over the past two years - driven by higher utilization and increased provider rates. Although recent WellSense’s insourcing efforts and contract negotiations may help moderate this trend, utilization is expected to remain elevated.

- Pharmacy costs are also expected to remain at elevated, double-digit levels. This is primarily driven by increased use of high-cost brand and specialty medications, based on projections from our pharmacy benefit manager (PBM) and Milliman.While anti-obesity GLP-1 drugs are excluded, a certain portion of members are expected to transition to diabetes-indicated GLP-1 therapies, where clinically appropriate, resulting in continued utilization of these high-cost medications. At the same time, manufacturer rebates have declined due to factors such as biosimilar adoption, changes in federal pricing policies, and adjustments related to the 340B program.

- Risk Adjustment:

- Updates to the 2027 CMS HHS Risk Adjustment model - based on Wakely’s simulation using 2025 experience - indicate a meaningful decrease in WellSense’s relative risk score. Rapid membership growth since 2024 has also lowered average risk levels due to shifts in member demographics. In addition, WellSense’s relatively lower average premium compared to the merged market increases the impact of risk adjustment transfers.

- Contribution to Surplus:

- The 2026 approved rates included a minimal contribution to surplus of 0.1%, well below the allowable 1.9%. The proposed 2027 rates reflect a return to a 1.9% contribution to surplus, which is necessary to maintain financial stability and ensure the continued availability of affordable coverage options.

Fallon Community Health Plan Inc.

Key Drivers for the Proposed Rate Change

The most significant drivers of the 25.7% rate change is summarized below:

- 5.1% rate increase due to a decrease in risk adjustment transfer receivable

- 8.5% increase to claims due to changes in base period allowed claims from 2024 to 2025 and impacts due to shifts in metal, age, and geography

- 3.3% increase to claim costs because of anticipated morbidity changes due to federal and state policy, such as the expiration of enhanced premium subsidies

- 2.4% for utilization and mix trends

- 3.7% for unit cost trends

- -0.7% reduction due to lower contribution to surplus

- 1.5% increase due to changes in taxes and fees such as the Exchange User Fee, PCORI, and MA State Assessment

Harvard Pilgrim Health Care, Inc.

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

See accompanying file called “Exhibit for Public Release” for additional detail.

- Medical Trend: A key driver of health insurance premium increases year-over-year is medical trend, which is comprised of inpatient, outpatient, and physician services. Medical trend includes both increases in the cost of the services provided by hospitals and physician groups and increases in the utilization and severity of these services by our members.

- For 2026 and 2027, Harvard Pilgrim expects there to be continued upward pressure on medical cost increases, driven by the higher inflationary environment and labor shortages that have led to providers requesting higher rates of reimbursement. While Harvard Pilgrim expects to successfully partner with hospitals and physicians across the state to moderate these cost increases, and continue to make quality care accessible for all, the increases are expected to be above historical levels.

- Harvard Pilgrim also continues to experience elevated medical utilization & severity trends. Utilization has increased across multiple categories of services and is not driven by any single event or service type.

- Pharmacy Trend: Pharmacy spend continues to put significant upward pressure on overall claim trend, particularly for brand drugs such as Immunomodulators, oncology drugs and other high-cost specialty drugs, and this is expected to continue in 2027. Note that as of January 2026, Harvard Pilgrim no longer covers GLP1 for weight loss indications; the reduction in expected future claim costs for this change in coverage is reflected in the filed rates.

- Risk Adjustment: Both actual and projected changes in the risk of Harvard Pilgrim members, relative to the market, results in a higher expected receivable for Harvard 1Pilgrim. This is helping moderate the increase, partially offsetting the medical and pharmacy trends.

- Other drivers of the rate change include a provision for the anticipated impact of the revised PACT Act and recently finalized prior authorization regulations, updated administrative cost assumptions, and the impact from the updated base period experience.

Health New England, Inc

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

- Health insurance premiums reflect the cost and usage of medical care and services. Health New England (HNE) has been impacted by increases in these areas due to higher costs and utilization of medical services and prescription drugs. As a result, our medical and pharmacy trends continue to rise.

- The largest driver of HNE’s 2026 requested rate increase is a rise in the costs of medical services and drugs. Pharmacy costs are expected to increase by 8.2% in 2027.

- This increase is driven by increased use of specialty drugs and the growth of new therapies. Members are also expected to use 3.4% more prescription drugs in 2027.

- Physicians and hospitals are facing economic pressures caused by supply chain shortages, overall inflation and continued workforce challenges. As a result, providers are seeking higher reimbursement for their services. HNE continues to be diligent but is routinely required to increase service reimbursement rates at levels that exceed the 3.6% cost control benchmark, established by the MA Health Policy Commission, to maintain its current provider network.

Mass General Brigham Health Plan, Inc.

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

...Several key factors are driving the proposed rate increase:

- Policy and Market Changes Impacting Affordability and Risk Pool

- The implementation of the federal law H.R. 1 also known as the One Big Beautiful Bill Act is driving significant shifts in how individuals and families qualify for coverage and what they pay for their health plans. Further, the expiration of enhanced premium tax credits has affected affordability, reducing the financial support that previously made health insurance more accessible for our members. These federal policy changes negatively affect the risk pool, through the loss of lower-risk members and limit access to more affordable plan options, particularly for our Health Connector members.

- We are seeing a growth of self-insured “level funded” small group options, from 2 percent in 2021 to over 11 percent in 2025 (based on the Center for Health Information and Analysis (CHIA) Enrollment Trends Databook as of September 2025 ). These products are medically underwritten which pulls small groups with favorable risk out of the merged market risk pool, leading to a deterioration of the fully insured merged market risk pool and worsening affordability for individuals and small businesses who remain in the merged market.

- Rising Cost and Utilization of Healthcare Services

- Industry-wide increases in the cost and utilization of healthcare services continue to reflect both regional and national trends. Trends are being driven by rising incidence of chronic conditions, as well as new medical technologies and treatments, which are improving outcomes, but often come at high costs set by manufacturers. This filing incorporates efforts to improve the effectiveness and efficiency of utilization management and care management processes through investment in greater integration between plan and provider from both a technology and a payment perspective.

- Accelerated Pharmacy Trends

- Pharmacy costs remain a significant driver of trend, particularly due to increased utilization of specialty medications and the introduction of new, high-cost therapies. For some conditions, such as diabetes, per-patient spending, rather than price alone has increased, due to more intensive treatment and management with higher cost treatments. Despite discontinuing cov erage for GLP-1s for weight loss, we continue to see rising utilization for diabetic GLP-1s as these treatments increasingly are being used to treat diabetes and expanded for other conditions. MGBHP has accelerated the use of formulary and pipeline management strategies aimed at reducing pharmacy spend by evaluating areas such as alternatives to clinical duplicates, including movement to biologic equivalents for some specialty medications and adjusting preference away from high-cost brands and generics.

- Investments in Access and Member-Centered Care

- The rate filing incorporates strategic investments to improve access to high-quality, affordable care. These include a robust women’s health portfolio, expansive behavioral health and mental health solutions, virtual primary care services, and digital tools designed to enhance member engagement and care coordination. Overall, the proposed rate change reflects a balanced approach to managing these cost pressures while continuing to provide comprehensive, high-quality coverage. Mass General Brigham Health Plan remains focused on mitigating cost increases through targeted pharmacy and care management initiatives, operational efficiencies, and disciplined administrative cost management, while investing in programs and innovations that improve affordability, access, and member outcomes.

Tufts Health Public Plans, Inc.

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

- • Medical Trend: A key driver of health insurance premium increases year-over-year is medical trend, which is comprised of inpatient, outpatient, and physician services. Medical trend includes both increases in the cost of the services provided by hospitals and physician groups and increases in the utilization and severity of these services by our members.

- For 2026 and 2027, THPP expects there to be continued upward pressure on medical cost increases, driven by the higher inflationary environment and labor shortages that have led to providers requesting higher rates of reimbursement. While THPP expects to successfully partner with hospitals and physicians across the state to moderate these cost increases, and continue to make quality care accessible for all, the increases are expected to be above historical levels.

- THPP also continues to experience elevated medical utilization & severity trends. Utilization has increased across multiple categories of services and is not driven by any single event or service type.

- Pharmacy Trend: Pharmacy spend continues to put significant upward pressure on overall claim trend, particularly for brand drugs such as Immunomodulators, oncology drugs and other high-cost specialty drugs, and this is expected to continue in 2027. Note that as of January 2026, THPP no longer covers GLP1 for weight loss indications; the reduction in expected future claim costs for this change in coverage is reflected in the filed rates.

- Risk Adjustment: Both actual and projected changes in the risk of THPP members, relative to the market, results in a higher expected payable for THPP, increasing the average rates. In particular, changes in member eligibility for state and/or Federal subsidies are expected to change the member mix and risk profile more negatively for THPP than the market.

- Other drivers of the rate change include a provision for the anticipated impact of the revised PACT Act and recently finalized prior authorization regulations, updated administrative cost assumptions, and the impact from the updated base period experience.

UnitedHealthcare Insurance Company

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

A rate change increase of 14.2% is necessary for 2027 renewals. This increase is necessary largely due to the following key drivers:

- Medical and pharmacy claim costs continue to increase, including but not limited to the following services which have seen significant increases:

- Outpatient Surgery

- Inpatient Surgery

- Infusion Services and Specialty Drug Costs

- Emergency Care Costs and over-utilization

- Mental Health/Behavioral Health Services

- Physician Office Visits

- Maternity Inpatient Services

- UHIC is required to pay payments into the ACA Risk Adjustment program. For 2025, we are projected to pay 2.2% of our premiums into the risk adjustment program, which reduces our 2027 rates by 3.6%.

- UHIC has faced increases to administrative expenses, driven by inflationary pressures.

- Historical rate levels have not fully kept pace with emerging experience, increasing the pressure on current rate proposals.

Advertisement