2027 Rate Changes - Indiana: +18.9% indy, +14.1% sm. group (preliminary)

Fri, 06/19/2026 - 5:29pm

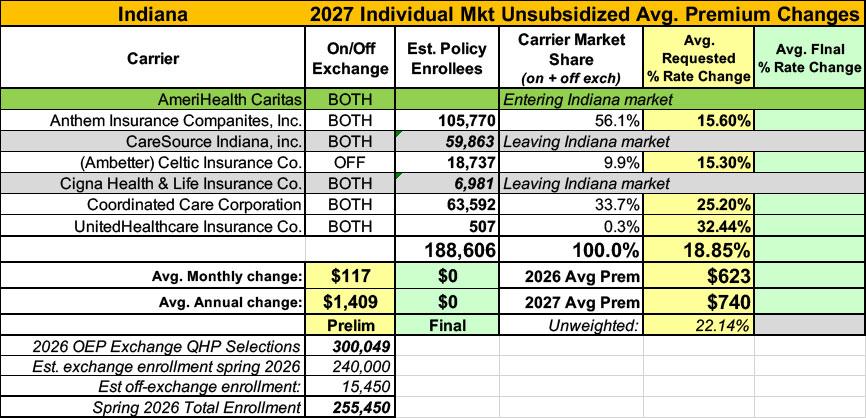

The first thing that's important to understand about the Indiana insurance market is that there are two carriers leaving the individual (ACA) market, and one possibly (?) leaving the small group market next year.

I had previously written about Cigna Health & Life Insurance pulling completely out of the ACA market across all states in 2027. In Indiana, Cigna only had around 8,600 ACA enrollees last year; this year, according to this article, it's down to fewer than 7,000.

CareSource is also pulling out of Indiana along with at least some other states as well. Again, according to this story, they have nearly 60,000 currently effectuated Hoosiers enrolled in their individual market policies.

Combined with the preliminary rate filings from the remaining four individual market carriers offering coverage next year found in the SERFF database, that puts Indiana's total current individual market size at around 256,000 people, which includes both on & off-exchange enrollees.

This is pretty concerning considering that that just over 300,000 Hoosiers signed up for coverage during the 2026 Open Enrollment Period...which itself was already down 59,000 from the 2025 OEP.

Even if you assume that only 6% of the enrollees are off-exchange, that still means that net effectuated ACA enrollment was likely down to perhaps ~240,000 as of March...which would be a 20% drop from OEP and a 16% drop vs. the same point a year earlier. Ouch.

Of course, this shouldn't be surprising given that net premiums skyrocketed by 85% this year for Indiana enrollees, due almost entirely to Congressional Republicans and the Trump Regime allowing the enhanced federal subsidies to expire back in December.

In any event, the resulting worsening of the risk pool, combined with other factors, has led Indiana individual market carriers to put in preliminary weighted average rate increase requests of 18.9% for 2027. If approved as is, that would mean unsubsidized enrollees would have to pay a whopping ~$1,400 more in premiums alone next year.

The only positive news is that there appears to be one carrier newly entering the Indiana market: AmeriHealth Caritas:

Anthem Insurance Companies, Inc. (also referred to as Anthem) has made an application to the Indiana Department of Insurance for premium rate changes for its fully ACA-compliant individual health plan products. This rate change will impact approximately 102,400 current Indiana insured members renewing in 2027 with Anthem. This filing includes an average rate change of 15.6%, excluding the impact of aging, effective January 1, 2027. At the individual plan level, rate changes range from 11.9% to 29.6%. An individual’s actual rate could be higher or lower depending on the geographic location, age characteristics, dependent coverage and other factors.

Financial Experience

Anthem expects the proposed rate change will cover projected medical trends and yield a medical loss ratio of 83.6%, meaning more than eighty-three cents of each premium dollar are expected to go to covering our members’ medical expenses and improving health care quality. This projected MLR of 83.6% exceeds the minimum MLR requirement of 80% as defined in the Affordable Care Act (ACA). In the event Anthem’s MLR is less than the Federal required minimum for a three year period, Anthem will refund the difference to policyholders, consistent with federal regulations.

Drivers of Rate Increase

One driver of premium rate changes is associated with the increased cost of benefit expense for this ACA compliant block. Increased cost of benefit expense is driven by increases in the price of services primarily from hospitals, physicians and pharmacies, coupled with members increasing their use of health care services, also called “utilization”. Increases in the price of services are driven by technological advances, new specialty medications, and a variety of other factors. Increased utilization is driven by member level utilization and selection patterns in the Guaranteed Issue, Community Rated ACA market.

Celtic Insurance Company is filing rates for the individual block of business, effective January 1, 2027. This document is submitted in conjunction with the Part I Unified Rate Review Template and the Part III Actuarial Memorandum.

This information is intended for use by the Indiana Department of Insurance, the Center for Consumer Information and Insurance Oversight (CCIIO), and health insurance consumers in Indiana to assist in the review of Celtic Insurance Company’s individual rate filing.

The results are actuarial projections. Actual experience will differ for a number of reasons, including population changes, claims experience, and random deviations from assumptions. In 2025, earned premium was $521.76 per member per month (PMPM). Incurred claims in 2025 were $388.19, or 74.40% of premium. Netting risk adjustment from the claims results in an estimated loss ratio (incurred claims net of estimated risk adjustment transfers, divided by earned premiums) of 83.62%. We expect unit costs to increase for 2027. Further, we have updated underlying experience for the single risk pool, expected administrative expense, and assumptions for federal risk adjustment. These factors, as well as changes to the assumed morbidity of the single risk pool and medical trend, result in a premium rate increase.

Medical trend, or the increase in health care costs over time, is composed of two components: the increase in the unit cost of services and the increase in the utilization of those services. Unit cost increases occur as care providers and their suppliers raise their prices. Utilization increases can occur as people seek more services than before. Additionally, simple services can be replaced with more complex services over time, which is known as service intensity trend. An example of service intensity trend would be the replacement of an X-ray with an MRI scan. Replacing the service with a more intense service causes the total cost of medical services to increase.

The proposed rate change of 15.3% applies to approximately 18,073 individuals. Celtic Insurance Company’s projected administrative expenses for 2027 are $107.69 PMPM. Administrative expense does not include $10.13 for taxes and fees. The historical administrative expenses for 2026 were $78.61 PMPM, which excludes taxes and fees. The projected loss ratio is 85.6% which satisfies the federal minimum loss ratio requirement of 80.0%.

Coordinated Care Corporation is filing rates for the individual block of business, effective January 1, 2027. This document is submitted in conjunction with the Part I Unified Rate Review Template and the Part III Actuarial Memorandum.

This information is intended for use by the Indiana Department of Insurance, the Center for Consumer Information and Insurance Oversight (CCIIO), and health insurance consumers in Indiana to assist in the review of Coordinated Care Corporation’s individual rate filing. The results are actuarial projections. Actual experience will differ for a number of reasons, including population changes, claims experience, and random deviations from assumptions.

In 2025, earned premium was $506.31 per member per month (PMPM). Incurred claims in 2025 were $482.33, or 95.26% of premium. Netting risk adjustment from the claims results in an estimated loss ratio (incurred claims net of estimated risk adjustment transfers, divided by earned premiums) of 93.57%. We expect unit costs to increase for 2027. Further, we have updated underlying experience for the single risk pool, expected administrative expense, and assumptions for federal risk adjustment. These factors, as well as changes to the assumed morbidity of the single risk pool and medical trend, result in a premium rate increase.

Medical trend, or the increase in health care costs over time, is composed of two components: the increase in the unit cost of services and the increase in the utilization of those services. Unit cost increases occur as care providers and their suppliers raise their prices. Utilization increases can occur as people seek more services than before. Additionally, simple services can be replaced with more complex services over time, which is known as service intensity trend. An example of service intensity trend would be the replacement of an X-ray with an MRI scan. Replacing the service with a more intense service causes the total cost of medical services to increase.

The proposed rate change of 25.2% applies to approximately 63,592 individuals. Coordinated Care Corporation’s projected administrative expenses for 2027 are $101.70 PMPM. Administrative expense does not include $16.14 for taxes and fees. The historical administrative expenses for 2026 were $86.75 PMPM, which excludes taxes and fees. The projected loss ratio is 85.0% which satisfies the federal minimum loss ratio requirement of 80.0%

UHIC will sell Individual policies with an effective date of January 1, 2027. The 2027 aggregate rate change as shown on the Unified Rate Review Template (URRT) is 32.44%. The rate change by product is 32.23% for UHC IND EPO and 32.86% for UHC IND EPO ADAV. Rate changes by plan are found in Worksheet 2, row 1.11 of the URRT. The quantitative impact for all significant factors driving the proposed rate change is shown in the table below. There might be small differences compared to the URRT due to rounding error.

Components of Rate Change

- Single Risk Pool Experience 10.9%

- Medical Inflation -1.4%

- Increased Utilization 4.7%

- Administrative Expenses 6.8%

- Market Morbidity 6.8%

- Other 1.4%

- Total 32.4%

Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes. Additional detail is provided below describing the significant adjustments driving the proposed rate change.

- Single Risk Pool Experience reflects actual emerging experience relative to that assumed in the development of PY2026 rates. Experience was more adverse than anticipated, contributing to upward pressure on rates.

- Medical Inflation represents the impact of changes in projected unit cost trends for medical services, including changes in reimbursement levels.

- Increased Utilization captures changes in the expected frequency and intensity of services utilized by members, independent of unit cost trends.

- Administrative Costs reflects changes in administrative costs, including taxes, fees, and other non-benefit expenses, from PY2026 to PY2027.

- Market Morbidity represents the projected shift in the underlying risk profile of the covered population. This includes an anticipated reduction in enrollment among healthier, lower-utilizing members and a corresponding increase in the proportion of higher-risk members. The morbidity impact also reflects expected effects of regulatory changes, including reduced subsidy eligibility for certain populations.

- Other reflects any changes to the rates not already captured above.

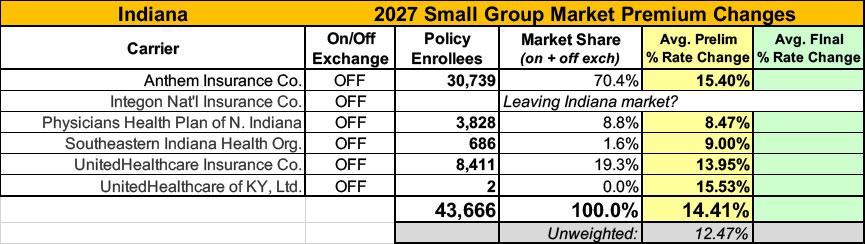

As for the small group market, I only found filings for five of the six carriers participating this year. I don't know whether Integon National is leaving the market or not (I can't find any evidence either way), but they only had around 1,000 enrollees last year. The remaining five are asking for weighted increases of 14.4%.

Advertisement